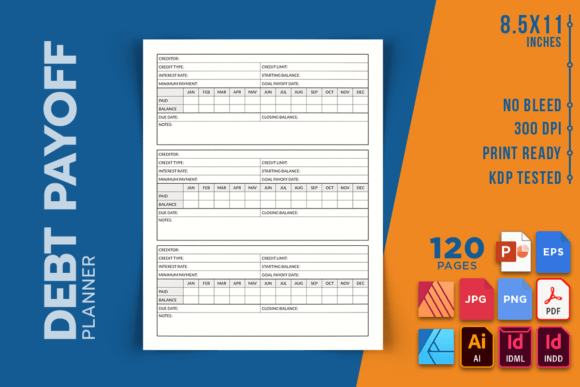

Debt Payoff Planner

Financial clarity rarely arrives by accident. For anyone juggling credit cards, student loans, car payments, or medical bills, the path to zero balances often looks like a tangled mess of minimum payments and interest calculations. A dedicated Debt Payoff Planner transforms that confusion into a structured, visual sequence of decisions and actions. It’s not a miracle cure; it’s a reliable framework that helps you see the full picture, prioritize effectively, and track real progress week by week.

This particular planner arrives as a professionally designed KDP interior—a print-ready PDF and editable source file package that puts 120 pages of structured debt payoff tools into your hands. Whether you plan to print copies for personal use, incorporate the design into a commercial journal line, or offer the planner as a coaching resource for clients, the underlying logic remains the same: organize, strategize, execute, and review. The difference lies in having a ready-made system that removes the heavy lifting of layout creation, letting you focus entirely on the financial content you’ll fill in.

Where a Dedicated Payoff Tool Fits Into Real Financial Workflows

Most people already engage with their money through spreadsheets, banking apps, note-taking software, or even sticky notes on a fridge. A Debt Payoff Planner doesn’t replace those; it sits at the center as a dedicated decision-making and tracking hub. Before you start using the planner, you might gather statements and log minimum payments into a digital app. During your active payoff phase, the planner becomes the physical anchor where you sketch out snowball or avalanche sequences, recalculate as interest shifts, and record actual payments. After a debt is cleared, the same pages serve as a motivational archive and a reference for future financial moves.

This workflow integration works because the planner forces you to condense scattered data into one portable, visual format. Instead of switching between five tabs on a screen, you open a single 8.5 x 11 inch spread, see your debt inventory at a glance, and map out the next three months without digital fatigue. The act of writing also taps into a deeper cognitive commitment—research consistently shows that handwritten planning improves goal follow-through.

Organizing Debt Information for Immediate Clarity

Before any payoff strategy works, you need to know exactly what you’re dealing with. Many people avoid this step because it’s emotionally heavy. The Debt Payoff Planner turns this initial confrontation into a neutral, guided process. Open the first section, and you’re presented with space to list each debt: creditor name, total owed, interest rate, minimum payment, and due date. There’s no judgment—just empty lines waiting for honest numbers.

This simple inventory can reveal hidden patterns. You might notice that three small debts carry negligible interest but drain your focus each month, or that one medical bill has a ballooning rate you never caught in your digital statements. When you physically write these figures, the relationships between debts become tangible. You start thinking about allocation not in abstract percentages but in real dollar amounts that correspond to the checkboxes and progress bars the planner provides.

The 120-page structure accommodates both simple and complex situations. If you have only two debts, your planner covers months of detailed tracking. If you’re managing multiple loans and credit lines, you won’t run out of room mid-year. The ample page count encourages consistent use without the anxiety of "using up" precious space too quickly.

Crafting a Payoff Strategy That Adapts Over Time

A fixed plan rarely survives contact with real life. You might intend to follow the debt avalanche method—targeting the highest interest rate first—only to face an urgent car repair that temporarily shifts your extra payments to a smaller balance for psychological relief. The Debt Payoff Planner doesn’t lock you into a single approach. It provides templates that let you sketch multiple scenarios, compare total interest saved under different orders, and adjust month by month.

Practical implementation works like this: In one section, you’ll find dedicated pages for strategy selection. Write out your proposed payoff order, estimate the number of payments required for each debt, and note any dates where extra income (tax refunds, bonuses, side gig earnings) could accelerate the timeline. Then, as months pass, use the monthly tracking pages to record what actually happened. Did you apply that bonus in full? Did you pause one debt to handle a medical deductible? The planner captures those pivots without making you feel like you failed. Instead, it reveals how flexible resource allocation keeps you moving forward.

Over time, you’ll notice that your strategy becomes more intuitive. The planner helps you internalize patterns—like the fact that paying an extra $50 on a 22% APR card yields a far greater long-term benefit than the same amount on a 5% student loan. You stop relying on online calculators and start trusting the numbers you’ve been tracking manually.

Tracking Progress and Maintaining Momentum

Motivation lags when results feel invisible. Paying an extra $200 toward a $10,000 balance barely moves the needle in your bank app, but inside a Debt Payoff Planner, that same action gets recorded with a visual marker. Many pages include mini-progress charts, payoff date countdowns, or coloring sections that make incremental wins feel significant. This isn’t about gamification for its own sake; it’s about creating a feedback loop that reinforces consistency.

Consider the psychological power of flipping back through three months of completed pages. You see not just the declining balances, but also the notes you wrote when you skipped a restaurant meal to throw more at a card, or the spike in payment when you sold unused electronics. The planner turns abstract discipline into concrete evidence of your choices. That archive becomes especially valuable during moments of doubt—when you’re tempted to take on new debt, revisiting the hard work already invested can be a powerful deterrent.

Integrating the Planner with Other Financial Tools

A physical planner doesn’t exist in isolation. It thrives when used alongside digital banking, budgeting software, and even conversations with a spouse or accountability partner. Here’s a realistic integration flow: Each week, you check your bank and credit card portals for recent transactions and updated balances. You then transfer the relevant numbers into the Debt Payoff Planner during a brief planning session. If you use a budgeting app like YNAB or EveryDollar, the planner becomes the strategic layer—defining which debt categories get extra funding—while the app handles daily expense tracking.

For couples, the planner can serve as a shared reference point. Instead of one partner managing all the numbers in a spreadsheet the other never sees, the planner sits on a desk or kitchen counter where both can review it. Discussing trade-offs—like whether to use $300 for a weekend trip or to knock out a store credit card—becomes easier when the full debt picture is visible on a single page.

Financial coaches and counselors can also integrate this tool directly into client sessions. Assigning specific pages as homework between meetings turns abstract advice into concrete actions. Since the interior file is provided with editable source formats—INDD, IDML, AI, PDF, and others—coaches can even customize a few pages with their own branding or exercise prompts before printing.

Quality and Usability Features That Support Long-Term Use

Design details determine whether a planner ends up filled cover to cover or abandoned after two weeks. This Debt Payoff Planner interior is created with daily use in mind. The 8.5 x 11 inch size provides enough room to write comfortably without being unwieldy on a desk or in a bag. No-bleed formatting means you can print it on any standard home or office printer, or send it to a print shop, without worrying about cut edges eating into your notes. The 300 DPI resolution ensures clean, crisp text and lines whether you view it digitally or produce a physical copy.

The 120-page length hits a practical sweet spot. It’s enough to document a full year of steady debt reduction without getting so thick that it becomes intimidating or difficult to bind. If you print it yourself, you can choose a binding method that fits your style—coil binding for a lay-flat experience, or a three-hole punch for a financial binder that also holds receipts and statements.

Because this is an interior-only product, you have complete freedom over the cover. You can design a professional cover that reflects your personal brand, a motivational image that speaks to your goals, or a minimalist look that blends into your workspace. If you’re a publisher or business owner, this flexibility allows you to market the planner under your own brand while relying on a tested interior structure.

Adapting the Planner for Different Roles and Scenarios

The versatility of a non-personalized interior means the same file serves multiple audiences. A freelance designer buying the editable source can rebrand it for a client in the personal finance niche. A productivity blogger might print copies for a workshop on financial goal-setting. A parent teaching a teenager about loan repayment can use simplified sections to create a learning tool. Because the content is debt-specific but not pre-filled, it adapts to student loans, business credit lines, mortgages, or medical debt without revision.

For small business owners, separating personal and business debt while using the same planning format simplifies management. One planner can be dedicated to business obligations, another to personal. The consistent layout reduces the mental switching cost when moving between contexts. Marketers and educators can pull excerpts or screenshots—permitted under standard commercial use terms for KDP interiors—to illustrate blog posts or course materials about financial planning.

Practical Implementation Workflow from Start to Finish

Getting started requires minimal setup. After purchasing the interior files, you download the high-quality PDF for immediate printing, or open the editable source files (INDD, IDML, AI, AFDESIGN, or PPTX) to make any modifications. If you plan to publish on Amazon KDP, you upload the provided PDF directly and pair it with your own cover design. For personal use, you print the pages you need—perhaps all 120 at once, or a smaller batch to test your workflow—and punch holes or bind them.

Begin the content by filling out the debt inventory. Spend 30 minutes gathering accurate numbers. Then move to the strategy pages: choose a payoff order, set target dates, and note any upcoming income boosts. Weekly, update the tracking pages with actual payments and any balance changes. Monthly, revisit the strategy section to adjust as needed. When you close an account, use the celebration pages or blank notes spaces to mark the win. This consistent rhythm transforms debt payoff from a stressful unknown into a predictable, manageable process.

By the time you reach page 120, the planner will contain a complete record of your journey. More importantly, you’ll have internalized habits and insights that extend far beyond the final zero balance. The Debt Payoff Planner thus serves not just as a task manager, but as a training ground for better financial decision-making in every area of your life.