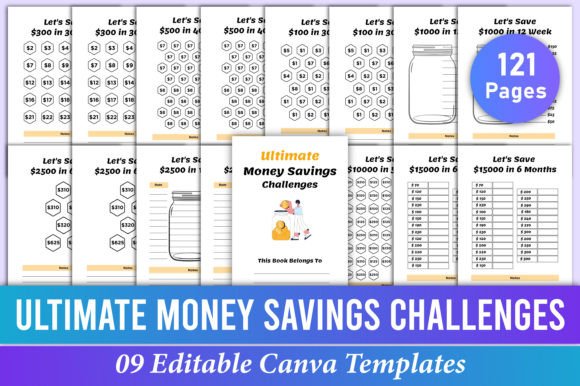

The Ultimate Book of Savings Challenges PDF: A Flexible Toolkit for Reaching Money Goals Without the Stress

Most budgeting advice sounds the same: cut out coffee, track every cent, live on a spreadsheet. But if you're earning a modest paycheck, juggling irregular freelance income, or simply feeling numb every time you open a banking app, that traditional advice rarely sticks. The real gap isn't knowledge — it's motivation and a system that actually fits a messy, real-life schedule. That's where the Ultimate Book of Savings Challenges PDF starts to make sense. It’s not a rigid financial lecture. It’s a collection of trackable, visual savings challenges paired with a printable logbook, all wrapped in an editable PDF you can use on a tablet, print at home, or keep in a binder on your kitchen counter.

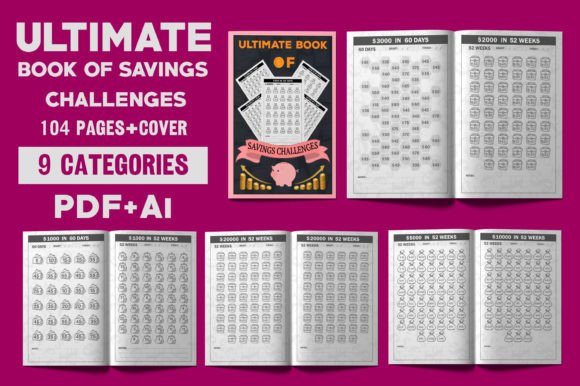

The core idea is deceptively simple: break a larger financial target — covering a wedding, a much-needed vacation, an emergency cushion, or just breaking a paycheck‑to‑paycheck loop — into small, satisfying steps. The file bundles nine distinct savings categories and a dedicated budgeting activities log, supporting specific goals like $20,000, $10,000, $5,000, $3,000, $2,000, $1,000, and even a quick $250 micro‑challenge. By coloring in or checking off squares as you go, you turn delayed gratification into a game you can see and touch. That tactile feedback loop matters more than any motivational quote.

Why a Printable Savings Challenge Works When Apps and Spreadsheets Fail

Digital budgeting apps often assume a steady paycheck and an already organized mind. But if you're a server, a rideshare driver, a new freelancer, or someone who pays bills with cash tips, the flow of money doesn't look like a neat pie chart. Typing numbers into a phone screen can feel disconnected from the actual money leaving your wallet. The Ultimate Book of Savings Challenges PDF bridges that gap by making the process physical and editable at the same time. You can type your progress directly into the PDF on a laptop, or print the pages and stick them on the fridge. When you see a row of 50 empty circles gradually fill up with pen marks, your brain registers a mini‑win every single time. That’s behavioral design, not just organization.

Another quiet advantage: the logbook section is built to capture spending triggers. Instead of just tallying numbers, the budgeting activities log asks you to note patterns — what time of day you impulse‑buy, what emotion preceded a splurge. This shifts the exercise from dry accounting to habit awareness. For low‑paid workers who can’t simply “earn more” overnight, spotting a $75 monthly leak on late‑night delivery apps can be the difference between never saving and building that first $1,000 buffer.

1. The Wedding or Vacation Saver on a Tight Timeline

If you’re planning a wedding that’s 18 months away and need $10,000, a blank notebook feels overwhelming. The $10,000 savings challenge inside the PDF gives you a clear map: 100 squares, each representing $100. On months when freelance work is flush, you might fill three squares. During a lean month, you fill one, but you still see the cumulative color spreading. You can circle the target date right on the page and adjust the editable PDF to reflect your own mini‑milestones — like paying the venue deposit by summer. For a vacation, the $5,000 or $3,000 tracker keeps the goal tangible without making you feel guilty about every latte. There’s also a $2,000 tracker that works beautifully for a solo weekend escape or a couple’s getaway, letting you save in $20 or $50 chunks.

2. The Low‑Income Worker Building an Emergency Net

When $500 feels impossible, the $250 or $1,000 challenges become lifelines. A home health aide, a retail associate, or a recent graduate working multiple part‑time gigs can start with the smallest tracker and treat each $10‑increment square as a quiet victory. The PDF includes a category specifically designed for irregular earners: instead of fixed weekly amounts, the trackers allow for flexible “pick an amount and color the corresponding box” style. On a week with overtime, you grab a higher‑value square. On a light week, you tackle a $5 square. By the end of the grid, you’ve stacked up a small fund that covers a car repair or a surprise medical copay. The psychological shift is enormous — you move from “I can’t save” to “I’m a person who has a safety net.”

3. Breaking a Specific Spending Habit Without Complete Deprivation

One of the smartest inclusions in this bundle is the budgeting activities log that pairs with the challenges. Let’s say you’ve identified that your biggest drain is online impulse buying after dinner. You don’t need to go cold turkey; you need a replacement behavior. You might print out the $1,000 challenge and commit that every time you resist a “wishlist” purchase, you move the would‑be amount into savings and fill a square. The log helps you track what time the urge hit, what you felt, and what you did instead. Over weeks, that data becomes a personal playbook. For a blogger, this log is also content‑rich material for a series about mindful spending. For a small business owner, adapting this tracking to separate personal and business splurges can reveal hidden profit drains.

4. Creators, Educators, and Coaches Teaching Financial Literacy

If you’re an educator running a high school personal finance workshop, a printable PDF you can distribute forever is gold. You can email the file to students, let them pick their challenge based on a part‑time job income goal, and have them fill it out over a semester. The editable cover page means each student can personalize their packet with their name and a photo of their goal — a guitar, a laptop, first‑month rent. For coaches who support clients through money mindset blocks, the nine challenge categories offer a ready‑made framework. You can start a client on the $1,000 emergency fund tracker, then graduate them to the $5,000 “freedom fund” challenge. Pairing the logbook with weekly check‑ins turns a generic PDF into a tailored coaching tool without paying for a custom app.

5. Side Hustlers and Gig Workers Managing Irregular Cash Flow

A freelance graphic designer may land a $3,000 project one month and earn $400 the next. Traditional monthly budgets buckle under that volatility. Using the printable $3,000 challenge, they can deposit a percentage of every invoice straight into a separate savings account and color in boxes proportionally. The editable PDF can be marked up digitally on an iPad with a stylus, which feels natural in a creative workflow. A rideshare driver might keep the printed $5,000 tracker in the glovebox, filling squares at the end of each shift when they reach a daily earnings threshold. These small rituals turn erratic income into visible progress, reducing anxiety about the slow months because the log shows cumulative momentum.

What Makes the Editable PDF Format a Practical Advantage

Many money tools lock you into an app ecosystem or require internet access. An editable PDF sits on your device — laptop, tablet, even a phone with a PDF annotator. You can type directly into the fields before printing, or fill it entirely on screen. The cover is also editable, which lets you brand it for a coaching program, add a personal motto, or simply label it “Lisa’s House Fund $20,000.” For a publisher or a blogger selling printables, this white‑label flexibility is a commercial asset. For an everyday user, it means you don’t have to copy pages manually; you can just print a fresh copy if coffee spills on the original. The file includes enough pages to cover multiple goals or repeat a challenge, so you’re not restricted to a one‑time use.

Understanding the Nine Savings Categories and the Logbook

The bundle organizes challenges into nine distinct pathways, each tied to a concrete goal amount. Instead of a single boring spreadsheet, you get dedicated trackers for $20,000, $10,000, $5,000, $3,000, $2,000, $1,000, and $250. The remaining categories incorporate themed challenges — one might focus on weekly deposits that grow incrementally (like saving $3 in week one, $6 in week two), while another might use a random‐pick method where you pluck a number from the grid and save that amount. This variety prevents monotony. The budgeting activities log sits alongside these trackers, with guided prompts: a space to write your “why,” a weekly spending snapshot, a reflection area for wins and slip‑ups. The log ties the challenges together so that you’re not just saving blindly; you’re understanding how your daily decisions feed into that colored grid.

What to Consider Before Downloading and Committing

Like any tool, the PDF works best when you align it with a realistic assessment of your cash flow. Before printing, take 20 minutes to scan your last two bank statements. Identify the gap between your necessary expenses and your income — the challenge amount should stretch you slightly but not set you up for failure. A $20,000 goal might be right for a couple saving for a down payment over three years, but disastrous for a single parent trying to squirrel away $800 a month from a tight paycheck. Start with the $1,000 or $2,000 tracker if you’ve never saved consistently before, even if your eventual target is larger. The habits form first; the total grows as income or circumstances shift.

Also, think about where you’ll keep the physical pages if you print them. Visibility matters. A tracker hidden inside a desk drawer rarely gets filled. Tape it to the bathroom mirror, hang it inside the pantry, or use an editable version as your tablet’s lock screen reminder. If you’re a marketer or entrepreneur, consider adapting the logbook sections into a client accountability tool — just ensure you’re not sharing the raw file in violation of any license terms; many purchasable PDF bundles allow personal and business use, but always confirm the included usage rights.

Finally, pair the paper with a separate, fee‑free savings account. The sense of separation — money “gone” from checking into the challenge account — reinforces the commitment. Even a digital envelope inside your banking app can work. The key is that the tracker mirrors real money movement. Otherwise, you risk coloring squares without actually moving the funds, which erodes trust in your own system.

Real Outcomes People Discover When They Use the Challenge Bundle

The most common shift users mention isn’t just a beefier bank balance. It’s a reduction in money‑related arguments with partners, because the fridge‑mounted tracker becomes a shared visual goal rather than a scolding spreadsheet. It’s the ability to say “yes” to a spontaneous dinner out without guilt, because the $1,000 challenge is already three‑quarters done and that night’s expense fits within the relaxed, pre‑planned wiggle room. It’s also a bridge for those who’ve never budgeted before to eventually adopt more detailed financial tools, because the logbook naturally builds awareness of where money goes.

For the creator selling this as a digital product, the editable nature means customers receive something usable instantly, even on mobile devices. No confusing software, no subscription. For the educator, it’s a semester‑long assignment that turns abstract concepts into a tangible artifact students can photograph and celebrate on social media, reinforcing positive peer influence around saving. Every niche that touches personal development — life coaches, wellness influencers, frugal living bloggers — can fold these trackers into their existing programs without reinventing the wheel.

The Ultimate Book of Savings Challenges PDF succeeds not because it invents some radical new financial theory, but because it translates the psychological power of micro‑progress into a format that actually fits the gaps left by conventional banking apps. Whether you’re aiming for a $250 cushion or a $20,000 milestone, the road suddenly looks less like a punishing climb and more like a series of small dots you can connect, one square at a time.